Money Guide Pro: How to Run a Short-Term Goal Plan

Click here to watch the recorded session.

Money Guide Pro is a great tool for retirement projections and goals-based financial planning in general, but can it be utilized to run a shorter-term, more cash flow based projection? The answer is yes, and the following article details my approach to structure a mathematically correct short-term goal plan - I also had opportunity to verify the accuracy with MGP's team of highly trained support, and that my approach produced meaningful results.

Step 1

Do quick retirement projections. First and foremost, a client with a short-term plan needs to verify that they are on track to retire on their terms at their current savings rate. If they are not, the first goal should be to increase their savings, and then determine the net taxable income that can be utilized towards short-term goals.

Step 2

Create the client > Click + Financial Goal Plan > select the College Zoomer conversation. This is the only financial goal plan conversation that DOES NOT require a retirement living expense goal. All other plans require the retirement tile in the goals section, and this, while important, messes with the results of the short-term plan.

Personal Info & Children. Enter as appropriate. These screens affect zero calculates in the plan, and should be entered like any other conversation.

Step 3

Goals. In the College Zoomer conversation, there are no required goal tiles - use as needed. The most common will be 'other', as it is the most flexible. As this is a short-term goal plan in software that utilizes a rolling plan year, it will always be more general than actual cash flow tools, as it does not operate by calendar/tax year. All goals are expressed annually, and the software will attempt to fund all goals at the start of the rolling plan year (not the end).

I recommend a 10 year plan as the minimum for short-term plans built in MGP. Keep your term in mind when building out the goals; for a 10 year plan, for example, your earliest goals should start in 2022, and your last goal should end in 2031. As you build, you can click the 'Timeline' button in order to access graphics that will assist you in entering the correct years to produce the length of plan you want.

Goals should still be expressed as after tax amounts.

Step 4

Investment Assets. This is where how you enter the plan alters the most significantly from a traditional long-term retirement plan entered in MGP. As opposed to considering these investment accounts, they will be entered as if they were streams of income.

First, if you've already run a retirement plan, you would alter those accounts to 'Not Used In Plan' (do not delete them, as this will delete the account across all plans.

Taxable Accounts. Then, you would account for all net, taxable streams of income by adding each as a 'taxable' investment account. The accounts can be entered with a balance reflecting the client's current checking or savings balance, or as a $0 current balance depending on the situation. Each account should be allocated as 100% cash.

Streams of income are accounted for as 'Annual Additions', and should be entered as net, pre-tax additions. In this case, 'net' refers to the client's paycheck less any retirement savings and all other pre-tax deductions, such as medical insurance. It does not mean net of federal and state taxes, as MGP will calculate taxes as an outflow on it's own (described later). You could choose to enter them as post-tax additions - just make sure that everything is lining up as you intended from an income and expense perspective.

In the example above, the client had plans for income streams from rentals, for which annual taxable additions were added and lined up with the timing on the goals screen as appropriate. In addition, he wanted to plan for reduced income after having children, as his wife would only plan on working part-time instead of full.

Savings. The trickiest part to model accurately in this short-term structure, is any savings that the client has a goal to complete towards short-term goals. The most accurate way to do so, is to reduce a spending goal by the savings amount, NOT as it's own goal. MGP will start with beginning value and then increase by additions, fund goals, and then show ending portfolio value. Thus, lowering the cash outflows will result in the client's savings.

In the example above, the client had a goal to save approximately $25,000/year pre-kids. To model this, basic living expenses were set to $75,000/year until kids, while annual income was approx. $100,000, resulting in a modeled savings of approx. $25k/year.

Step 5

Results. The current and recommended scenario results will still run a monte carlo simulation, however, because everything is 100% cash, there can only be two results: 0% or 99%. Either it works, or it doesn't.

Step 6.

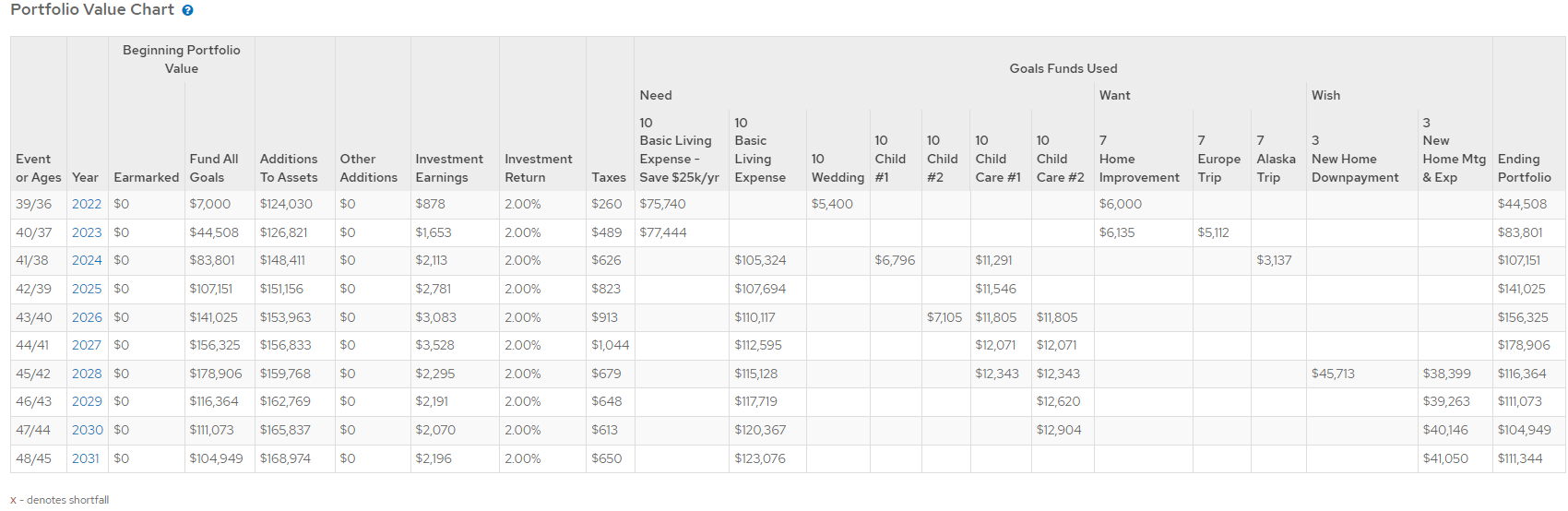

Meaningful results. From here, click the Explore menu > then go to Combined Details. This is where it all comes together, and you are able to demonstrate a meaningful, year by year projection of income vs. expenses, and cross reference it with the ending balance (savings).

This same chart will demonstrate any projected short-falls in goal funding, as it still prioritizes Needs over Wants and Wishes.

Final Tips

- Timing is critical - make sure to check the timeline graphic as well as the Combined Details chart to ensure that you are lining up income streams with expenses accurately.

- The recommended scenario will try to invest assets according to the risk tolerance setting if you do not lock accounts. For this reason, it is practical to not utilize recommended, and simply use current scenario graphics and results. This can also be altered in the what-if worksheet to maintain 'current' investments instead of rebalancing.

- The year account additions start and stop cannot be altered in the What-If worksheet; for this reason, if the timing of goals changes, which also alters the timing of various income streams, it may be necessary to copy the whole plan and create a new one to model the differences, as opposed to utilizing the what-if worksheet.

As always, feel free to submit a Help Ticket with additional questions, or email Nicola directly at nicola@garrettadvisors.com.